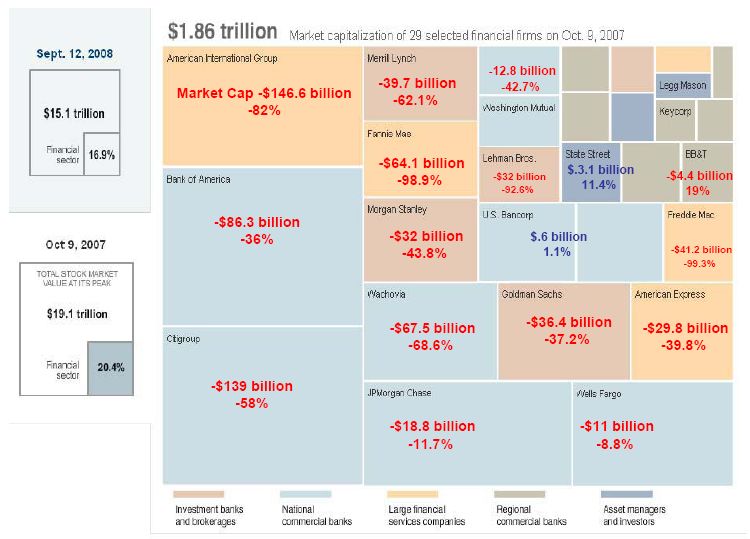

Change in value of 29 select financial firms over the past 12 months.

.jpg "delta")

Excerpted from Michael Berry’s morning notes.

We personally have lost some money on paper, but have also invested in the past week while things have been “on sale”, in preparation for the launch of the Tax-Free Savings Account (TFSA) on 1-Jan-08. Don’t wait until the end of 2009 to start your money working for you tax-free, plan to max your TFSA right away! Our plan is to max our TFSA at the start of each year ($5k per person), and buy a basket of medium-risk stocks or income trusts spread between a few sectors (real estate, power generation, oil, financial) that pay out reasonable yield (>5%, preferrably >10%), and a) long-term collect tax-free income, but b) short-term use dividend re-investment (DRIP) to purchase additional shares each month/quarter to compound our returns until we are ready (or need) to switch them over to generating cash. In 5 years, assuming no more than one or two of them crater, they could be throwing off quite a bit of cash!

Now if only they would introduce income splitting for people younger than 65 …

{kind=link}

lisa d - dan, could you break this tfsa thing down for me?

sounds good but a little over my head thus far! 🙂

thanks

xoxox

Dan - Hi Lis,

Sure – here’s the expanded version.

The TFSA, like the RRSP, is just a “shell” that you can put investments in. RRSP contributions are “before tax”, in that you get to reduce your taxable income by the amount of your contribution each year. Money grows inside tax-free, but then withdrawals are taxed as income when you eventually take $ out, hopefully during rtirement.

TFSA’s are “after tax”, as they don’t generate a tax deduction. However, any withdrawal you take is tax-free. So you could just put your TFSA $ into a high interest savings acct and make 3% tax-free. Or you could buy gold bars or mutual funds, hope they go up, and sell them tax-free in the future.

I argue the best use of these is to buy high yield invesments like income trusts and bank stocks that have DRIPs (where the monthly or quarterly dividends buy additional units commission-free), so your investments compound tax-free until you need the income. Then you turn off the DRIP, and instead of buying additional stock each month or quarter, you take the cash out tax-free each month.

Of course, the drawbacks are that you have to find the $ to put into the TFSA in the first place, and the risk is that the stocks can go down in value, or reduce or stop paying dividends, which is why you have to diversify and keep an eye on them, but the potential for income generation is huge. If you’re diligent and put in your $5k each year ($10k per couple), each year’s money could earn you ~$80 per month (assuming you find something that yields 10%), before compounding. That’s $400 per month after 5 years (again before compounding), assuming dividends aren’t cut, stocks don’t crater, etc. And that’s tax-free. To take home an extra $400 a month after tax, you’d have to make ~$10,000 more a year at your job!

Auntee Jennee - I think I may have missed out on the Fullerton investment gene. *sigh*

Shannen - I hope Jaia inherits the gene from Dan, because this Fullerton is also lacking in that department so she wouldn’t be getting any financial know-how from me.

Angelo Bucciero - Hi Dan,

I have the same plan, I want to invest 10% of my household income in CIBC, BMO and Scotia (because they offer DRIPs and SPP), I want to put those shares that I buy every month in a TFSA and I want the fractional shares that I would be getting from those DRIPs to be added to my TFSA so that they grow in a tax free enviornment and that these fractional DRIPs don’t impact my $5000 limit. I explained this to a financial advisor from IG and she said I can recieve into my TFSA the dividends as cash but not as shares! Whats the difference if I get X$ in dividends or X% of a share instead? But she insisted it can’t be done.

How are you setting yourself up to have your DRIPs grow in your TFSA?

Thank you